You’ve probably heard some version of these classics:

The Advice That Didn’t Age Well

- “Just work hard, stay loyal, and the company will take care of you.”

- “Buy a house as soon as you can. Renting is throwing money away.”

- “Never talk about money. It’s private.”

- “Credit cards are dangerous. Pay cash for everything.”

This was the money starter pack for a lot of Boomers and Gen X—and much of it worked in a world where:

- Wages and housing were closer together.

- Stable jobs with pensions actually existed.

- College didn’t cost a small mortgage.

- The internet wasn’t constantly trying to sell you something.

That world is gone.

But the scripts are still echoing in family group chats and holiday dinners.

Let’s sort out which old-school money rules broke, which still hold up, and what a modern, realistic upgrade looks like.

Broken Rule #1: “Loyalty to Your Company Will Be Rewarded”

For your grandparents, this rule made sense:

- Stay 30 years with one employer.

- Get regular raises, a pension, maybe a gold watch.

- Retire with predictability.

Today, the math is different:

- Real wages for many jobs have barely moved in decades.

- Pensions have been replaced by DIY retirement accounts.

- Layoffs can hit even profitable companies.

Staying put can actually cost you money.

Studies keep finding that people get their biggest pay bumps by switching jobs, not waiting around.

Modern upgrade:

> “Be loyal to your skills, not to any one company.”

What this looks like:

- Regularly updating your resume and LinkedIn—even when you’re not job hunting.

- Asking for raises based on market data, not just time served.

- Being willing to leave if a workplace won’t grow with you.

Your career is a business. You’re the asset.

Broken Rule #2: “Buying Is Always Better Than Renting”

Once upon a time:

- Houses were cheaper relative to income.

- 30-year mortgages locked in low payments that felt manageable.

- You could realistically stay in one place for decades.

Buying became a one-size-fits-all badge of adulthood.

Today:

- In many cities, home prices have exploded compared to local wages.

- School and job opportunities are more spread out.

- Many people need flexibility to change cities or countries.

Buying is still powerful—but not automatically smarter.

Modern upgrade:

> “Buy when it supports your life and math, not just your ego.”

Questions to ask now:

- Am I likely to stay in this city for at least 5–7 years?

- After taxes, maintenance, and fees, is buying actually cheaper than renting?

- Do I have savings left after the down payment, or will I be house-poor?

Renting is not “throwing money away.” It’s paying for flexibility, maintenance, and lower risk.

The real money sink is buying something you can’t comfortably sustain.

Broken Rule #3: “A Degree Guarantees a Good Job”

Your grandparents might’ve worked their way through college on a part-time job. That’s… not how tuition works anymore.

Now:

- Degrees can cost more than a house.

- Some fields are saturated.

- Others don’t require a degree at all, just relevant skills.

A diploma still helps, but it’s not a golden ticket—it’s a tool.

Modern upgrade:

> “Education is an investment. Treat it like one.”

Ask before committing:

- What’s the average starting salary in this field?

- What’s the total cost of this degree, including interest on loans?

- Are there cheaper paths—community college, bootcamps, apprenticeships, certifications?

The right question isn’t “Should I go to college?” but “What’s the least expensive path to the career I want?”

Sometimes that’s a four-year degree. Sometimes it’s not.

Broken Rule #4: “Never Talk About Money”

Old logic:

- Talking about money is tacky.

- It causes conflict.

- It’s private.

New reality:

- If workers don’t share salary info, companies can quietly underpay.

- If couples don’t talk about money, they fight about it later.

- If families don’t talk about money, kids repeat the same mistakes.

Silence protects systems, not people.

Modern upgrade:

> “Talk about money with the right people, in the right ways.”

This looks like:

- Asking coworkers you trust about pay ranges.

- Having regular ‘money dates’ with your partner.

- Being honest with friends when you can’t afford something instead of silently swiping a card.

You still don’t owe the internet your bank balance. But you owe yourself informed decisions, and that often requires conversation.

Broken Rule #5: “Cash Only. Avoid Credit Completely.”

Many older relatives see credit cards as pure evil. Why?

Because they watched people wreck their lives with them.

Totally fair.

But the modern economy runs on credit scores:

- Landlords check them.

- Car and home loans are priced by them.

- Sometimes even employers glance at them.

Avoiding credit entirely can backfire.

Modern upgrade:

> “Credit is a power tool. Learn to use it safely.”

Basics that still protect you:

- Never put more on a card than you can pay off in full this month.

- Automate at least the minimum payment to avoid late fees.

- Track your utilization (aim to use under ~30% of your limit).

Using credit wisely can mean cheaper loans, better housing options, and less stress later.

The goal of older advice—don’t drown in debt—is still right. The method just needs an update.

Old Rules That Still Slap (With Tweaks)

Not everything from back in the day is outdated. Some advice is timeless—just needs translation.

Still Good: “Live Below Your Means”

The core idea:

> Spend less than you earn so you have a cushion.

In an era of easy credit and constant ads, this is more crucial than ever.

Modern twist:

- Use tech (budgeting apps, account alerts) to see where your money actually goes.

- Focus on big levers (housing, car, subscriptions), not just skipping lattes.

Still Good: “Have an Emergency Fund”

Medical bills, layoffs, breakups, surprise moves—chaos is timeless.

Modern twist:

- Aim first for 1 month of expenses, then 3, then more.

- Keep it in a separate high-yield savings account you can access easily but don’t touch casually.

Still Good: “Don’t Co-Sign Lightly”

When you co-sign, you’re saying: “If they don’t pay, I will.”

That hasn’t changed.

Modern twist:

- Only co-sign if you could afford to make the payments yourself without wrecking your life.

- Put agreements in writing, even with family.

Culture Shift: Experiments vs. Forever Decisions

Your grandparents grew up in a world of:

- “One career for life.”

- “One city for life.”

- “Buy once, hold forever.”

Our world is more:

- Career zigzags.

- Remote work and relocation.

- Rapid tech and industry changes.

So our money strategy needs more optionality:

- Renting can be smart while you experiment with cities or careers.

- Keeping a bigger emergency fund gives you power to walk away from bad jobs.

- Diversifying income (even a small side hustle) adds safety your grandparents didn’t need as much.

You’re not flaky for not wanting a 30-year lock-in on everything. You’re adapting to your environment.

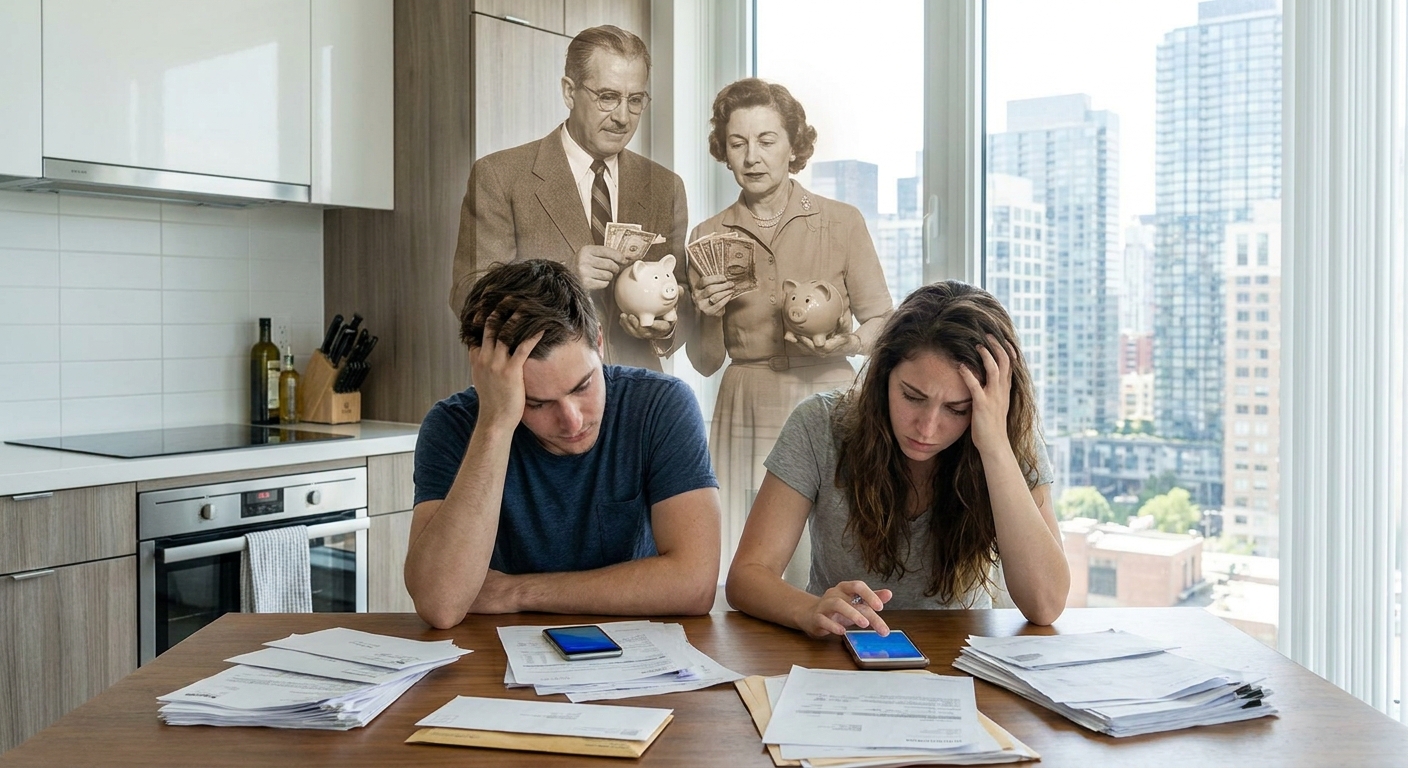

How to Respect Their Experience Without Copy-Pasting Their Plan

Money can get tense across generations because:

- They faced real hardship and want to protect you.

- You’re facing a financial landscape they never had to navigate.

Both realities can be true.

Here’s a simple framework:

- Ask for stories, not just rules.

- “What money mistake do you wish you’d avoided?”

- “What was your first big purchase?”

- “How did your parents talk about money?”

- Translate the principle to today.

- “Don’t use credit” → “Avoid toxic, high-interest debt, but build healthy credit.”

- “Work hard and be loyal” → “Work hard and build skills that keep you employable.”

- Design your own map.

- Use their lessons as inputs, not commandments.

You’re not betraying your grandparents by adjusting to reality. You’re doing exactly what they did: trying to give your future self a better shot.

The New Core Money Rules

If you strip away all the noise, a modern starter pack might look like this:

- Spend less than you earn—but don’t expect willpower alone to do that. Automate what you can.

- Build 1–3 months of expenses as a buffer before you worry about optimizing investments.

- Use credit strategically: build a strong score without carrying high-interest balances.

- Talk about money with people you trust so you’re not guessing in the dark.

- Invest in skills and adaptability, not just loyalty and degrees.

- Make big commitments (house, car, loans) match the life you’re actually living, not the one your grandparents lived.

You can honor the past and update the playbook.

Their world was typewriters and pensions. Yours is algorithms and side hustles.

The money game changed. You’re allowed—actually, you’re required—to change your strategy too.